Accelerating Wealth: How Borrowing to Invest Can Supercharge Your Portfolio

For investors looking to build wealth faster, borrowing to invest can be a smart and powerful strategy. By using someone else’s money, (the bank’s), you can amplify your portfolio growth while also benefiting from tax deductions on the interest payments.

This approach isn’t new. Affluent investors and business owners have used it for decades because it allows their own money to keep working elsewhere while borrowed funds build wealth in the market.

The Basic Setup

Here’s a simplified example for Ontario:

- Loan amount: $100,000 (interest-only loan)

- Loan rate: 4.5%

- Investment return: 9% annually

- Marginal tax rate: 30%

- Time frame: 2 - 4 years minimum, longer if you choose not to sell

You borrow $100,000, invest it in a diversified portfolio (mutual funds or segregated funds), and pay only the interest each month. The principal is repaid when you sell the investment.

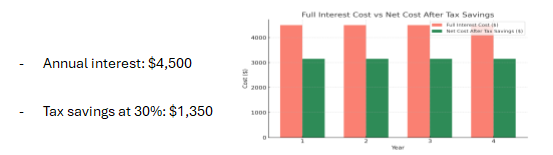

The Tax Advantage

The interest cost on money borrowed for non-registered investments is tax-deductible:

This means your real borrowing cost is much lower than 4.5% once the tax refund is factored in - effectively just 3.15% after-tax.

How the Investment Grows

We’ve assumed:

- 3% of the portfolio generates dividends/interest each year → taxed annually

- 6% of the portfolio grows as capital gains → taxed only when you sell

This keeps annual taxes low, allowing most of the growth to compound tax-deferred until the end.

Four-Year Illustration

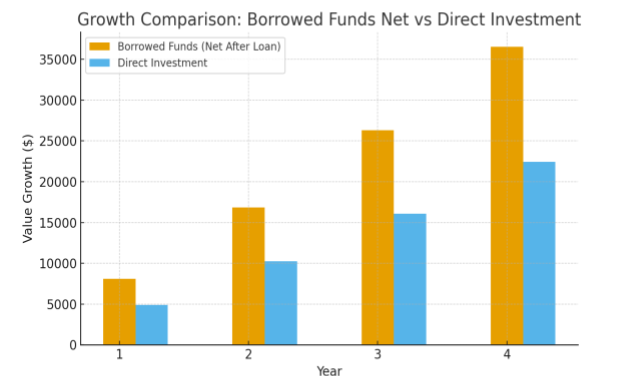

Here’s how $100,000 invested at 9% could grow using borrowed funds:

Year 1: End Value = $108,100

Year 2: End Value = $116,856

Year 3: End Value = $126,321

Year 4: End Value = $136,553

How It Compares to Simply Investing the Payments

What if, instead of borrowing, you just invested the same annual interest cost - 4,500 per year - at the same 9% return?

Because you’re using someone else’s money from day one, leveraging helps accelerate wealth far faster than just investing your own cash flow.

Key Considerations

- Time frame: Best suited for 2 - 4 years minimum. Longer terms allow more compounding and tax deferral.

- Tax efficiency: Only dividends/interest are taxed yearly. Capital gains tax is deferred until the end.

- Cash flow commitment: You must be able to handle the monthly interest payments comfortably.

- Market risk: Returns must outpace borrowing costs. A diversified portfolio and longer time frame help.

The Bottom Line!

Borrowing to invest can significantly accelerate your wealth if done correctly, with:

- Tax savings reducing your borrowing costs

- Leverage boosting your portfolio growth using someone else’s money

- Deferral of taxes on most gains until you sell

This is a smart strategy when you have the right risk tolerance, time horizon, and cash flow.

If you want to see whether this approach fits your financial plan, talk to us today. We can help you model the numbers and guide you every step of the way.