Mortgage Lender Insurance vs. Standalone Life Insurance

If you’ve recently bought a home or are reviewing your financial protection, you’ve probably heard about “mortgage lender insurance” (often offered by your bank) and standalone life insurance. While they both aim to help protect your mortgage, they work very differently — and it’s important to understand those differences.

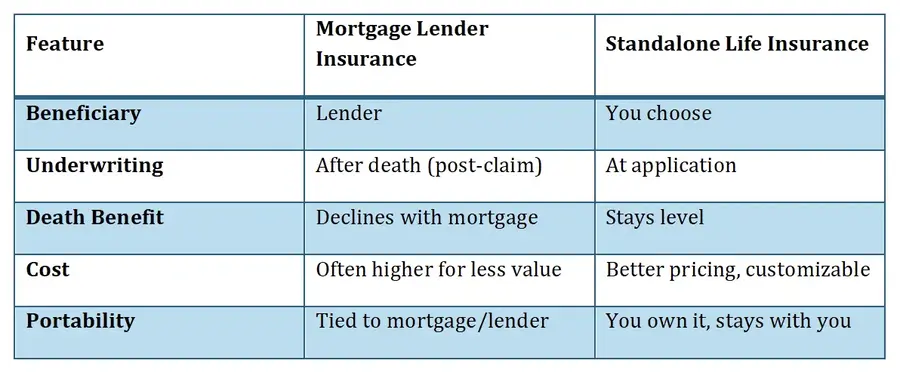

1. Who Gets the Money (Beneficiary Designations)

- Mortgage Lender Insurance: The bank is the beneficiary. If you pass away, the payout goes straight to the lender to pay off the mortgage.

- Standalone Life Insurance: You choose the beneficiary — usually your spouse or family. They can use the money however they need: mortgage, bills, education, etc. It gives your loved ones flexibility.

2. Underwriting Timing

- Mortgage Lender Insurance: Often uses post-claim underwriting, meaning they only fully assess your health after a claim is made. If they find an issue at that time, they may deny the claim.

- Standalone Life Insurance: Uses underwriting at time of application. Your health is reviewed upfront, so once you’re approved, the policy is secure. No surprises down the road.

3. Death Benefit Amount

- Mortgage Lender Insurance: The payout declines over time — as your mortgage balance drops, so does the amount of insurance. But your premiums stay the same.

- Standalone Life Insurance: The death benefit stays level. If you buy $500,000 of coverage, your family gets $500,000 — whether you pass away tomorrow or 20 years from now.

4. Cost Differences

- Mortgage Lender Insurance: Can seem convenient, but it’s often more expensive for the value provided. It’s one-size-fits-all and may not account for your actual health/lifestyle.

- Standalone Life Insurance: Usually offers better value, especially if you're healthy. Rates are based on your personal profile, and you may lock in a lower premium for longer.

5. Summary